Dubai’s hospitality story has always been told in terms of scale; new hotels, new brands, new skylines rising from reclaimed land. Yet the most consequential development of the next decade may not be a hotel at all. It is infrastructure. And it is quietly repricing everything.

With over $35 billion committed to the expansion of Al Maktoum International Airport (built to handle 150 million passengers in its first phase and up to 260 million at full capacity) Dubai is not just expanding aviation – it is reorganizing its own geography. Pair that with the imminent arrival of commercial air taxis operated in partnership with Joby Aviation, and what emerges is a city actively engineering a new definition of prime location.

For luxury hospitality brands, the implications are structural. The question is whether they are reading this as a logistics story or a brand strategy story. The ones treating it as the latter are already moving.

The Joby Aviation flying taxi takes flight in Dubai (Image Credit: Dubai Media Office)

Eight minutes changes everything

From 2026, electric air taxis will connect Dubai International Airport to Palm Jumeirah and Downtown Dubai in approximately eight minutes. The same journey by road, in peak traffic, takes 40. Vertiports are going in at DXB, near Dubai Mall, and at Atlantis The Royal. Over 30 existing hotel helipads are being upgraded to accommodate the new aircraft alongside helicopters.

A guest who lands at DXB, steps into an air taxi, and touches down on a hotel rooftop eight minutes later, has had an experience before they’ve even checked in. The brand lives inside that journey—the altitude, the city below, the seamlessness of it—whether the hotel engineered it or not. That is a fundamentally different arrival than handing someone a welcome drink after an hour of highway traffic.

But brand managers have questions. Which properties have vertiport access? Which can build the eight-minute transfer into their arrival narrative as a signature, not a footnote? In ultra-luxury segments, where time and privacy are valued as acutely as design or F&B, these questions are already influencing property selection. The brands that answer them first will define the category.

Network position is the new address

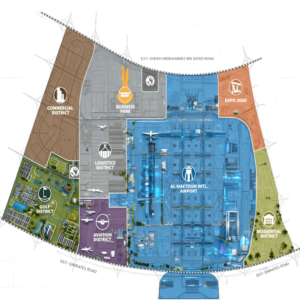

If air taxis are reshaping short-distance movement, Al Maktoum International is reshaping the macro geography of the entire city.

The airport’s full build-out anticipates a migration of Emirates and flydubai in the 2033–2035 window. When that happens—and the scale of commitment makes it a when, not an if—the center of international arrival moves southwest. Dubai South becomes the new front door.

Districts that currently carry a secondary-market perception, Palm Jebel Ali, Expo City, Dubai South itself, move directly into primary arrival flows. Property in that corridor is still trading at roughly 50% below Downtown prices. That gap reflects today’s infrastructure reality. It will not reflect 2033’s.

Nakheel’s Palm Jebel Ali projects and the branded residences rising around Expo City are bets on a specific infrastructure timeline, and the position is well-reasoned. The airport connects to a 14-station automated people mover, a new metro line, and Etihad Rail. For hotel operators and branded residence developers, the transitional pricing window is a function of timing. It closes as infrastructure visibility increases, and that visibility is increasing now.

Network position meaning connectivity to airports, vertiports, transit corridors, mobility nodes now carries as much strategic weight as physical address. A property’s postcode matters less than where it sits in the city’s emerging mobility architecture.

Visual map of Dubai South 2040 plan (Credit: Noorain Alam)

Dubai is running this play alone

Singapore’s Changi remains the world’s benchmark for airport experience, but it does not reorganize Singapore’s intra-city hotel hierarchy. Charles de Gaulle’s modernization expands capacity. It does not reprice arrondissements. NEOM has run eVTOL pilots with Volocopter; its hospitality ecosystem remains early-stage.

Dubai is doing something none of them are: expanding aviation capacity at 260-million-passenger scale, deploying urban air mobility at commercial scale, and growing luxury hospitality inventory simultaneously, with deliberate integration between all three. These initiatives compound each other in ways that sequential or siloed infrastructure development doesn’t. No comparable market is running this combination.

When speed becomes the story—and when it isn’t enough

There is a tension in infrastructure-led luxury positioning worth naming directly.

As connectivity becomes embedded in the value proposition, location risks being evaluated through efficiency metrics alone: transfer time, node proximity, seamlessness of arrival. But luxury has never derived its authority solely from efficiency. Cultural depth, atmosphere, the sense that a place exists on its own terms; these are not decorative layers on top of the product. They often are the product.

Two risks follow.

The first is hierarchy compression. When multiple districts are simultaneously upgraded through infrastructure integration, the scarcity premium attached to a prime address flattens. If everywhere is eight minutes from the airport, the address stops doing the same work. The second is brand coherence: a property that leads with frictionless arrival is making a promise. If the physical environment and service philosophy don’t match that register, the infrastructure becomes a setup the hotel can’t fulfill.

The counterargument is grounded in how Dubai has always operated. The Burj Al Arab was not discovered. It was engineered, and then the experience was built around the engineering. For a globally mobile UHNW segment, minutes saved and friction removed carry real economic and psychological value. Engineering time efficiency may be luxury’s most current expression – for this audience, at least.

Infrastructure amplifies hospitality advantage. It works best as a foundation, not the entirety of what a brand is asking its guests to pay for.

Ongoing construction of Palm Jebel Ali, Dubai

Time as a luxury asset

Dubai is building the physical infrastructure of a specific brand promise: that for the right guest, time, friction, and distance are solvable problems. The brands that will define luxury in Dubai by 2033 are the ones treating infrastructure connectivity as a core strategic asset now. Before it is fully priced in and before the arbitrage window closes.

By 2033, prime location in Dubai will not rest solely on views or waterfront access. It will depend on how seamlessly a property integrates into the city’s mobility architecture and whether that integration sits underneath an experience genuinely worth arriving for.

The infrastructure is being built regardless. The question is which brands will build their strategy around it, and which will discover it has already reorganized the market around them.

Ishanee Patra

-

Ishanee Patra is a luxury hospitality professional and MBA graduate in Luxury Brand Management, with international experience spanning Europe and Asia. She writes on the strategic evolution of experiential luxury, with a focus on how infrastructure, cultural hospitality, and destination branding are shaping the future of global luxury markets—with Dubai at the centre of that conversation.

- Aekta Kapoor (2)

- Aleyssandra Mendosa (1)

- Anuj Puri (3)

- Arvind Vijaymohan (1)

- Ashok Som (5)

- Ashutosh Limaye (1)

- Deepali Nandwani (19)

- Eva Pavithran (1)

- Gargi Guha (4)

- Gina Mathew (1)

- Ishanee Patra (1)

- Jenifer Willig (1)

- Joanne Pereira (4)

- Jordan Phillips (1)

- Kishor Pate (1)

- L.Aruna Dhir (4)

- Lauren Mote (1)

- LuxuryNext Team (205)

- Megha Puri (10)

- Mitch Ritter (3)

- Nishant Bangar (3)

- Nolan Lewis (17)

- Radhika Singh (1)

- Sanjana Chauhan (68)

- Shibani Dasgupta (1)

- Soumya Jain (3)

- Sue Stephenson (1)

- TheLuxury NextTeam (17)

- Veronique Poles (1)